The Rate Cut Ripple Effect: A Deep Dive into the Winners and Losers

The Financial Landscape Shifts: What the Latest Interest Rate Cut Means for You

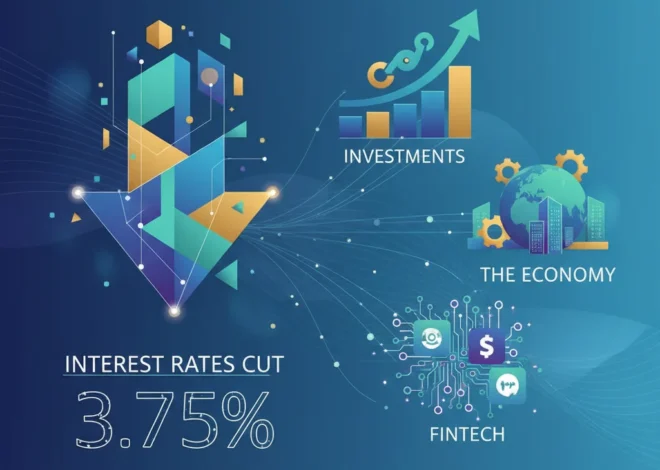

In a move that sent ripples through the financial world, the Bank of England has trimmed its key interest rate from 4% down to 3.75%. While a quarter-point reduction might seem small, this adjustment to the lowest level since February 2023 is a significant signal from the central bank. It’s a carefully calibrated decision designed to influence the entire economy, from the cost of a business loan to the returns on your savings account. But what does it truly mean? An interest rate cut is never a universally positive event; it’s a complex economic lever that creates a distinct set of winners and losers.

This decision isn’t just a headline for financial news channels; it has tangible consequences for households, investors, and business leaders. It alters the calculus for investing, changes the dynamics of the stock market, and reshapes corporate strategy. In this comprehensive analysis, we will dissect the multifaceted impacts of this monetary policy shift. We’ll explore who stands to gain from cheaper borrowing, who will feel the pinch of lower returns, and how you can strategically position yourself in this evolving economic environment.

Understanding the ‘Why’: A Primer on Central Banking and Monetary Policy

Before we can identify the winners and losers, it’s crucial to understand why a central bank like the Bank of England cuts rates in the first place. The primary mandate of most central banks is to maintain price stability (i.e., control inflation) and support maximum sustainable employment. The interest rate, often called the “base rate” or “policy rate,” is their most powerful tool.

This base rate is the interest rate at which commercial banks can borrow from the central bank. It acts as a benchmark, influencing the entire spectrum of interest rates set by commercial banks for mortgages, business loans, and savings accounts. When the central bank cuts this rate, it’s typically for one or more of the following reasons:

- To Stimulate Economic Growth: Lower rates make it cheaper for businesses to borrow money for expansion, new equipment, and hiring. For consumers, it reduces the cost of mortgages and other loans, encouraging spending and investment.

- To Combat Deflationary Pressures: If inflation is too low or there’s a risk of deflation (falling prices), a rate cut can encourage spending to push prices back up toward the target rate (usually around 2%).

- To Ease Financial Conditions: In times of market stress or economic uncertainty, a rate cut can provide liquidity and support to the financial system, boosting confidence in the broader economy.

This recent cut suggests the Bank of England is prioritizing economic stimulus, perhaps in response to data indicating a potential slowdown. As the Bank’s own Monetary Policy Report often details, these decisions are based on a vast array of economic forecasts and data points.

The Winners’ Circle: Who Benefits from Cheaper Money?

A lower interest rate environment directly benefits those who owe money or are looking to borrow. The effects are widespread, creating a clear group of winners.

1. Borrowers (Households and Businesses)

This is the most direct and obvious beneficiary. Homeowners with variable-rate or tracker mortgages will see an almost immediate reduction in their monthly payments, freeing up disposable income. For businesses, the cost of capital decreases. This makes it more attractive to take out loans to invest in new projects, upgrade technology, or expand operations, which can lead to job creation and economic growth. This is particularly crucial for capital-intensive industries and startups in the fintech space that rely on funding for scaling.

2. The Stock Market

Equity investors often celebrate rate cuts. There are two primary reasons for this. First, lower interest rates make safer investments like bonds and savings accounts less attractive, pushing investors toward the higher potential returns (and higher risk) of the stock market. This increased demand can drive up stock prices. Second, for the companies themselves, lower borrowing costs can translate into higher profits. Furthermore, in valuation models used in finance, future earnings are discounted at a lower rate, which mathematically increases the present value of a stock.

3. Growth-Oriented Companies

Companies in high-growth sectors like technology, biotechnology, and financial technology are often significant winners. These firms typically reinvest their earnings back into the business rather than paying dividends and often rely on debt to fuel their rapid expansion. Cheaper debt means more fuel for their growth engine. This environment fosters innovation and can accelerate the development of disruptive technologies.

Below is a summary of how different sectors might react to a rate cut, based on their business models.

| Sector | Potential Impact of a Rate Cut | Reasoning |

|---|---|---|

| Technology & Fintech | Positive | Lower cost of capital for R&D and growth; higher valuations for future earnings. |

| Real Estate & Construction | Positive | Lower mortgage rates stimulate housing demand and construction activity. |

| Consumer Discretionary | Positive | Consumers have more disposable income from lower loan payments, boosting spending on non-essential goods. |

| Utilities & Staples | Neutral to Positive | These are often seen as “bond proxies.” Their stable dividends become more attractive compared to lower bond yields. |

| Financials (Banking) | Negative to Neutral | Net interest margins can be compressed, though higher loan volume may offset this. |

The Other Side of the Coin: Who Feels the Pinch?

For every borrower celebrating a lower payment, there’s a saver or investor who is earning less. The costs of a rate cut are just as real as the benefits.

1. Savers and Retirees

This group is the most direct loser. The interest earned on savings accounts, money market funds, and certificates of deposit will fall, reducing a key source of low-risk income. This disproportionately affects retirees and other conservative investors who rely on the interest from their savings to cover living expenses. The quest for yield becomes significantly harder, potentially forcing them to take on more risk than they are comfortable with. According to analysis from financial experts, a prolonged low-rate environment can severely erode the purchasing power of cash savings over time.

2. The Banking Sector

The impact on the banking industry is nuanced but often negative. Banks make money on their “net interest margin” (NIM) – the difference between the interest they earn on loans and the interest they pay out on deposits. When rates fall, this margin often gets squeezed. While they can lower the rates on savings accounts, they are often already near zero, leaving little room for further cuts. Meanwhile, the rates on their loan portfolios decrease, compressing profitability. While lower rates might spur more loan demand, the reduced profitability on each loan can be a significant headwind.

3. Pension Funds and Insurance Companies

These institutions have long-term liabilities they need to fund, such as pension payments or insurance claims decades in the future. They typically invest in a large portfolio of high-quality government and corporate bonds to match these liabilities. When interest rates fall, the yields on new bonds they purchase are lower, making it much harder to generate the returns needed to meet their future obligations. This can lead to pension funding deficits and pressure on insurance premiums.

4. The National Currency

In the world of international finance, capital flows to where it can earn the highest return. A rate cut makes holding a country’s currency less attractive to foreign investors, as they can earn a better yield elsewhere. This reduced demand can cause the currency’s value to depreciate relative to other currencies, making imports more expensive for domestic consumers and businesses.

Hollywood's Endgame: Decoding the High-Stakes M&A Battle Reshaping Entertainment

The Investor’s Playbook: Navigating the New Low-Rate Reality

An interest rate cut is not just an economic event; it’s a call to action for investors and business leaders to reassess their strategies. Complacency is not an option.

- For Equity Investors: The focus may shift towards “growth” stocks (like tech) over “value” stocks. Sectors that benefit from lower consumer borrowing costs, such as real estate and consumer discretionary, may also see increased interest. Dividend-paying stocks can also become more attractive as a source of income. Sophisticated trading strategies might involve rotating capital into these favored sectors.

- For Fixed-Income Investors: The challenge is finding yield without taking on excessive risk. This may involve looking at longer-duration bonds (which come with more interest rate risk), corporate bonds instead of government bonds, or international bonds from countries with higher interest rates.

- For Business Leaders: This is a prime opportunity to review corporate debt. Refinancing existing loans at a lower rate can free up significant cash flow. It’s also a favorable time to seek capital for strategic investments in technology, infrastructure, or acquisitions that can drive future growth.

This is a pivotal moment in economics, where a single decision creates a cascade of effects. Financial markets are complex, dynamic systems, and the full impact of this rate cut will unfold over the coming months. Global economic outlooks will need to be adjusted as other central banks decide whether to follow suit or diverge in their policies.

Drax's Power Play: Why an Energy Giant's Move into Data Centres is a Game-Changer for Investors

Conclusion: A Delicate Balancing Act

The Bank of England’s decision to cut interest rates is a powerful move designed to steer the economy toward a path of stable growth. However, it is a double-edged sword. It provides welcome relief for millions of borrowers and can act as a potent stimulant for the stock market and corporate investment. Yet, it simultaneously penalizes prudent savers, challenges the business models of banks and pension funds, and can weaken the national currency.

Understanding where you stand in this equation of winners and losers is the first step toward making informed financial decisions. Whether you are an investor adjusting your portfolio, a business leader planning your next move, or a homeowner managing your budget, the ripple effects of this rate cut will undoubtedly reach you. The key is not to react emotionally, but to understand the underlying economic forces at play and adapt your strategy accordingly.

Related Posts

The Great Cool-Down: What November’s Inflation Report Means for the Economy, Your Investments, and the Future of Finance

Interest Rates Cut to 3.75%: What This Pivot Means for Your Investments, the Economy, and Fintech